Reflecting on the joy of the holiday season always brings with it gratitude. One of the most important pieces of my business is working with an office that always makes it a priority to come together as a team throughout the year to lift up our neighbors in need and give back to our communities. Our collective gratitude runs deep, and spreading some love and support within our community is the best way we can celebrate everything we are thankful for.

This year our holiday food drive brought in $1,372 and 1,422 pounds of food for Volunteers of America Western Washington food banks. These numbers are all thanks to friends and clients like you. Thank you for your generosity! The current need in our area is high, and our local food banks need all the help they can get.

Next, we had the absolute joy of helping bring some Christmas magic to homeless/housing-insecure youth in our area. We partnered again this year with Washington Kids in Transition, who work with social workers in Edmonds School District schools (includes the communities of Edmonds, Lynnwood, Brier & Mountlake Terrace) to collect wish lists from homeless/housing insecure students living in shelters, tents, cars, transitional housing or other temporary housing and partners with the community to fulfill those wishes. The brokers in my office all came together and we adopted the wish lists of 24 local youth, who would have otherwise gone without this holiday season.

The rest of the year, Washington Kids in Transition provides emergency closets (coats, diapers, toiletries, etc.), hotel vouchers, utility assistance, rental deposits, and recently started a teen mentorship program. This new program is in high demand, but does not yet have reliable funding, so we decided to also raise funds for that as well over the holiday. We raised a total of $3,815 for this new program, which helps teens learn basic life skills as well as have fun activities they otherwise wouldn’t have access to.

Another holiday staple at my office is putting together volunteer groups at Christmas House and also Holly House this year. Both organizations are local non-profits (100% volunteer-run) that provide opportunities for qualifying, low-income parents to select free holiday gifts for their children. This is always an amazing time helping families in need have a joyful Christmas.

You can access any of the links above to learn more about these organizations or to donate yourself. As we head into 2025, our commitment to giving back to the community that we serve will remain a cornerstone of our business. Here’s to a happy, healthy, and heartwarming 2025 and beyond.

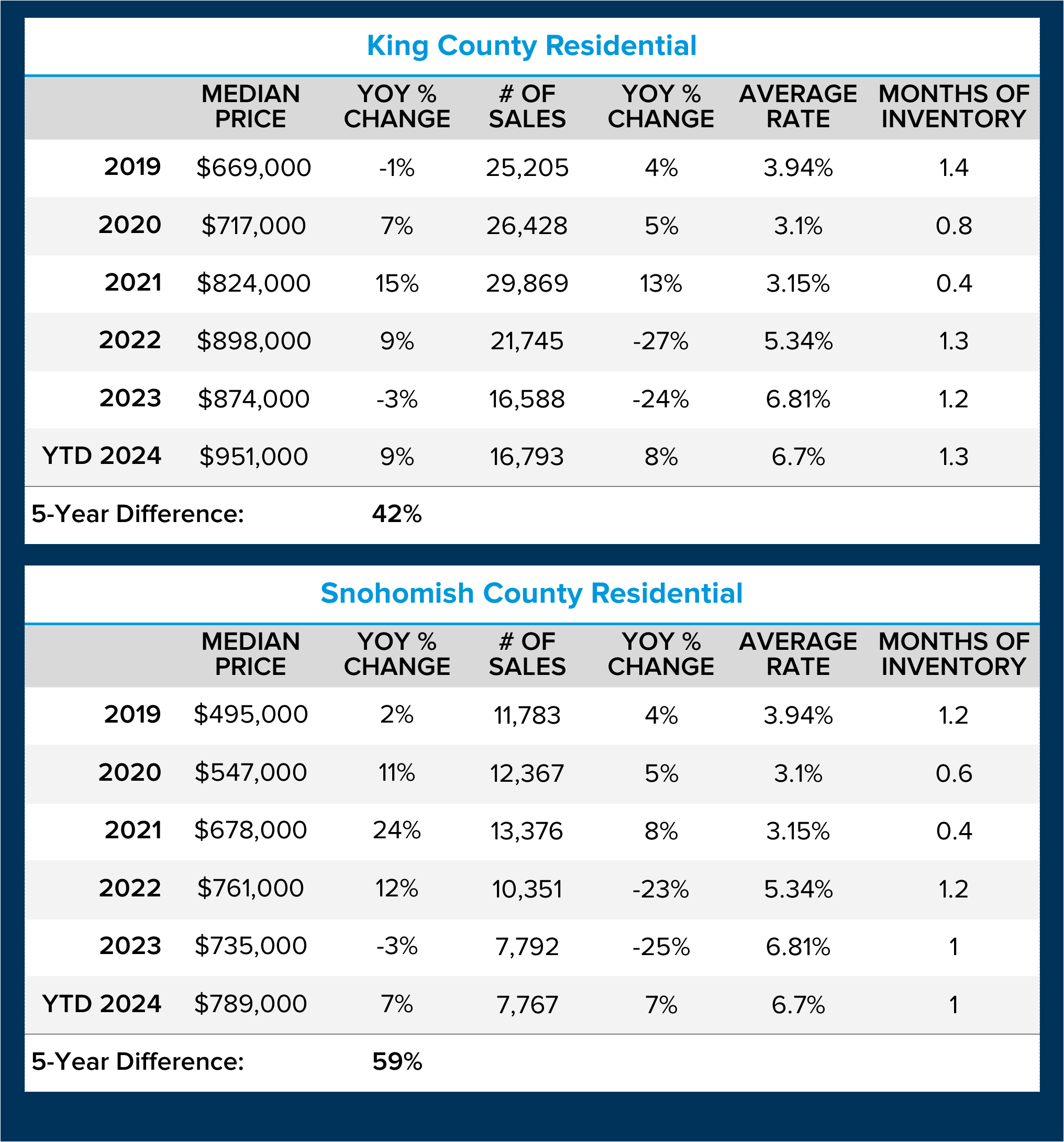

As we head into the holidays and mark the final stretch of the year, I wanted to report on the 2024 real estate market and where we might be headed in 2025. To set the stage, I must mention the ride that it has been over the last five years. Since 2019, we have experienced some key market factors that have influenced market activity and prices.

2019 was a year of recovery after the market corrected in 2018 (due to the Seattle Head Tax), and we all know what happened in 2020. The pandemic threw the real estate market into a frothy uptick from mid-2020 to mid-2022, fueled by work-from-home moves and historically low interest rates. Sales counts and price appreciation were ” off the charts,” specifically in 2021. Once interest rates climbed over 5% in the spring of 2022, price appreciation capped, started to correct, and sales declined. Since then, prices have recovered and stabilized, and the sales count has slowly started to increase.

After reviewing the last 10 years of closed sales, we are down about 25% YTD in King County and 30% in Snohomish County from a normal average closed sales rate. This has remained stubborn due to the lock-in effect that the previous low rates have created. For example, many homeowners who purchased or re-financed to obtain a rate of 3-4% are holding tight to their monthly payments. This has caused many people to stay in homes that don’t ideally fit their lifestyle due to wanting to keep the monthly payment and overall affordability.

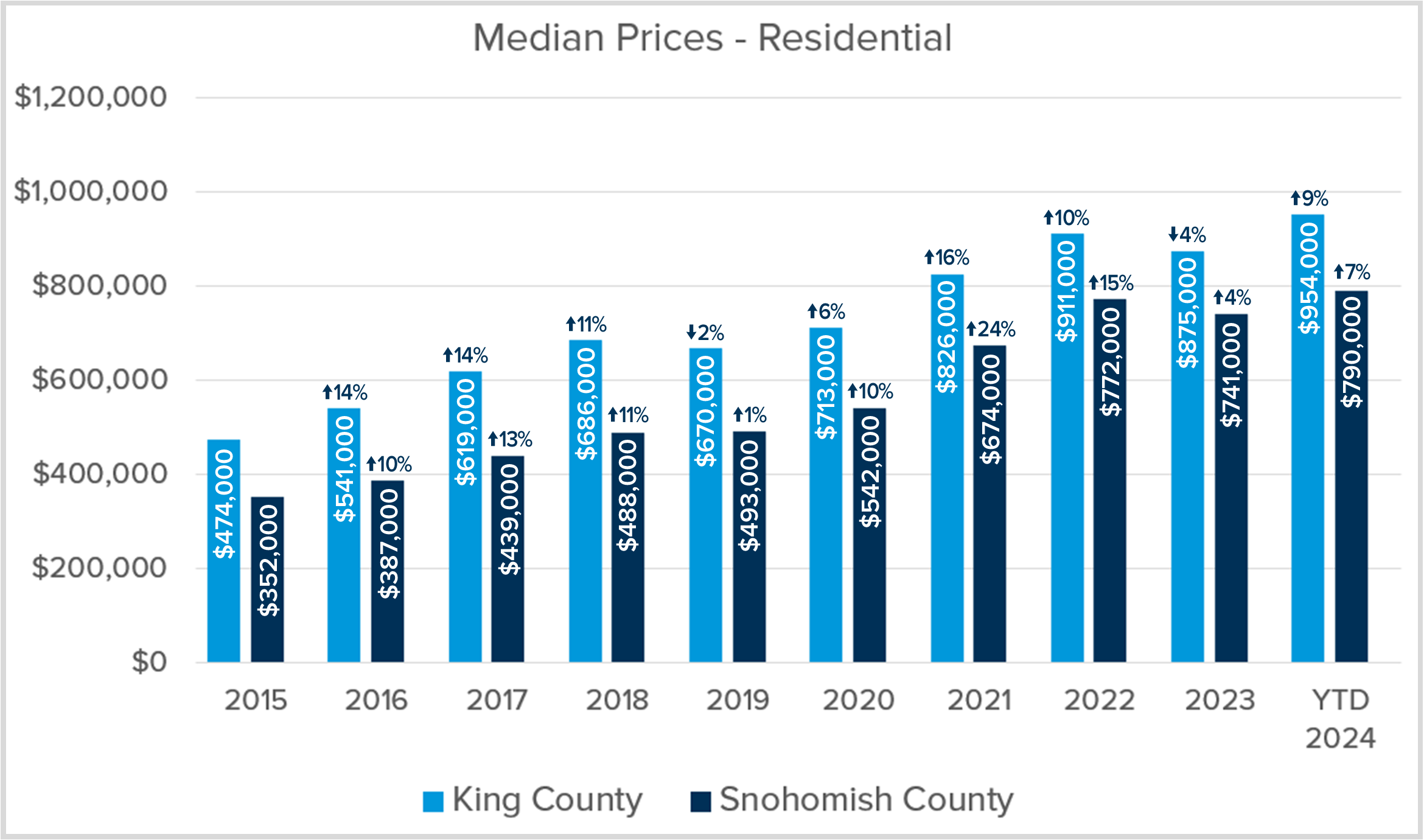

This has created tight inventory, which has insulated prices and helped the market recover from the 2022 correction. The dance between rates and low inventory is directly related, and despite rates being higher in 2024 than they were in 2022, prices remain strong. A seller’s market is defined by 0-2 months of inventory (if no new homes came to market, we would sell out of homes in this amount of time), a balanced market is 2-4 months, and a buyer’s market is 4+ months. Over the last 5 years, we have primarily been in a seller’s market. This has caused prices to increase by 59% in Snohomish County over the last 5 years and by 42% in King County.

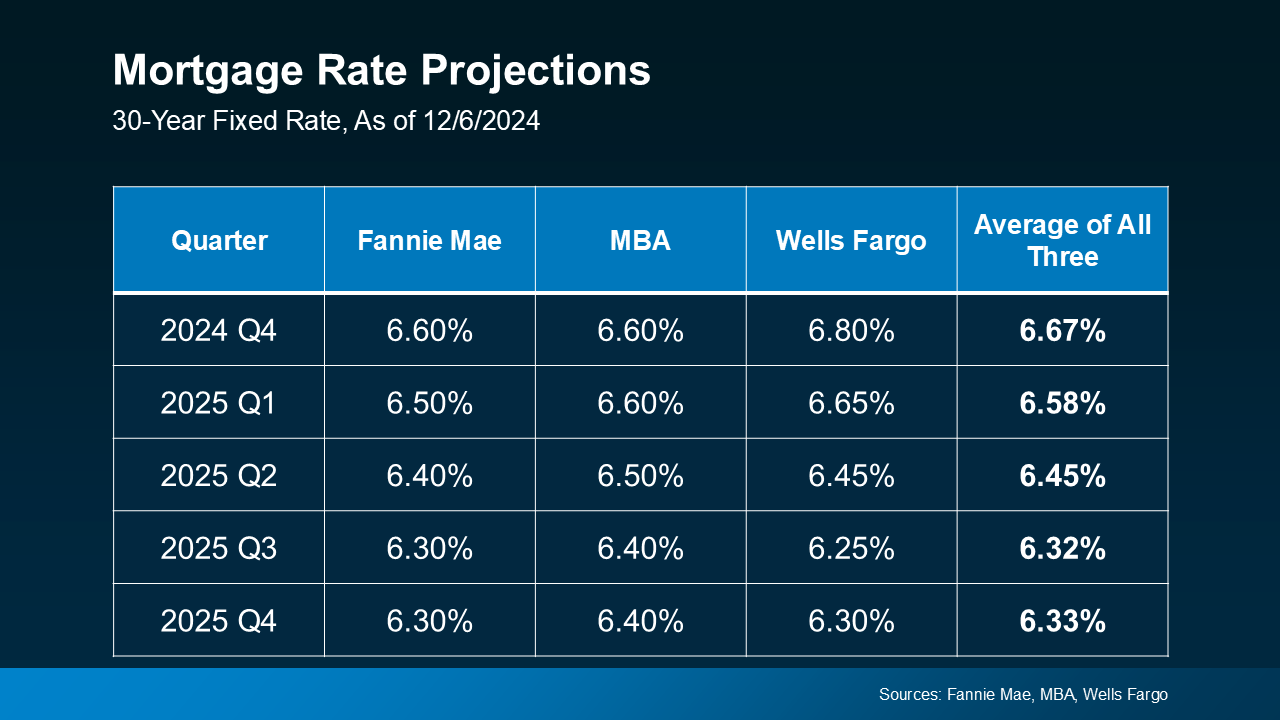

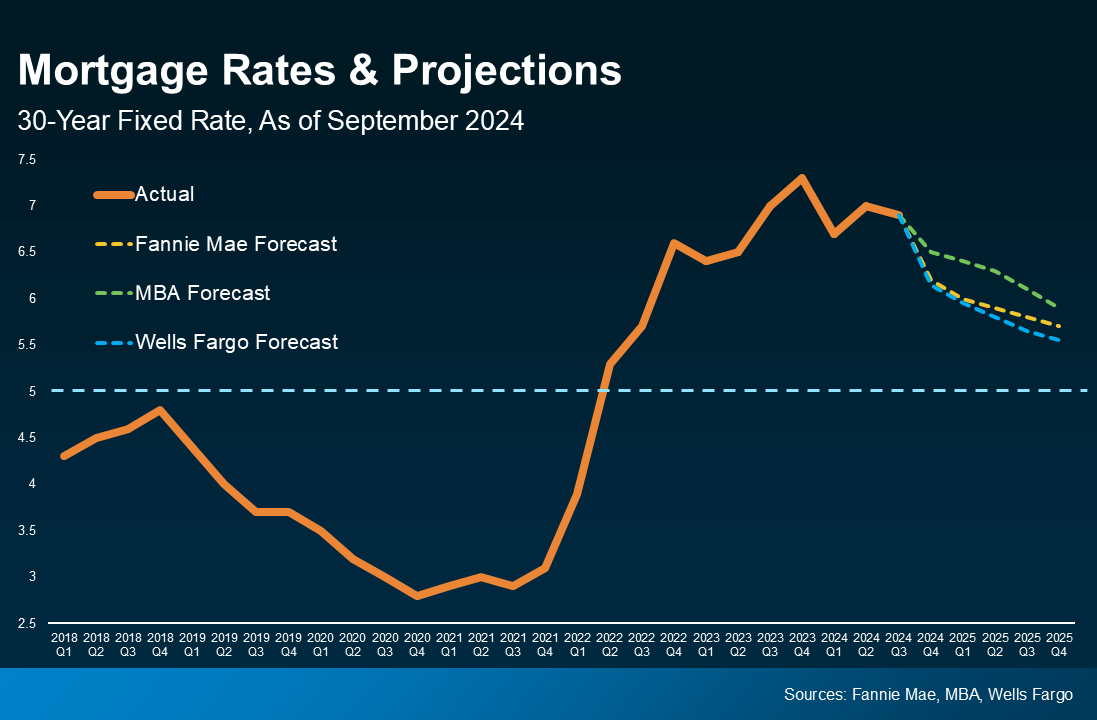

The age-old principle of supply and demand has had the most significant impact on prices despite volatile interest rates. Several experts predict that interest rates will slowly decrease throughout 2025. As you can see from the chart below, we will not return to the historic levels we saw in 2020-2021 (we may never). As would-be sellers contemplate the lock-in effect vs. what they want/need out of their housing and line it up against interest rates, we should see a gradual increase in closed sales in 2025 over 2024. The market is slowly starting to accept this new normal. Also, in some cases, moves cannot be delayed due to life circumstances, and the lock-in effect is not a driver.

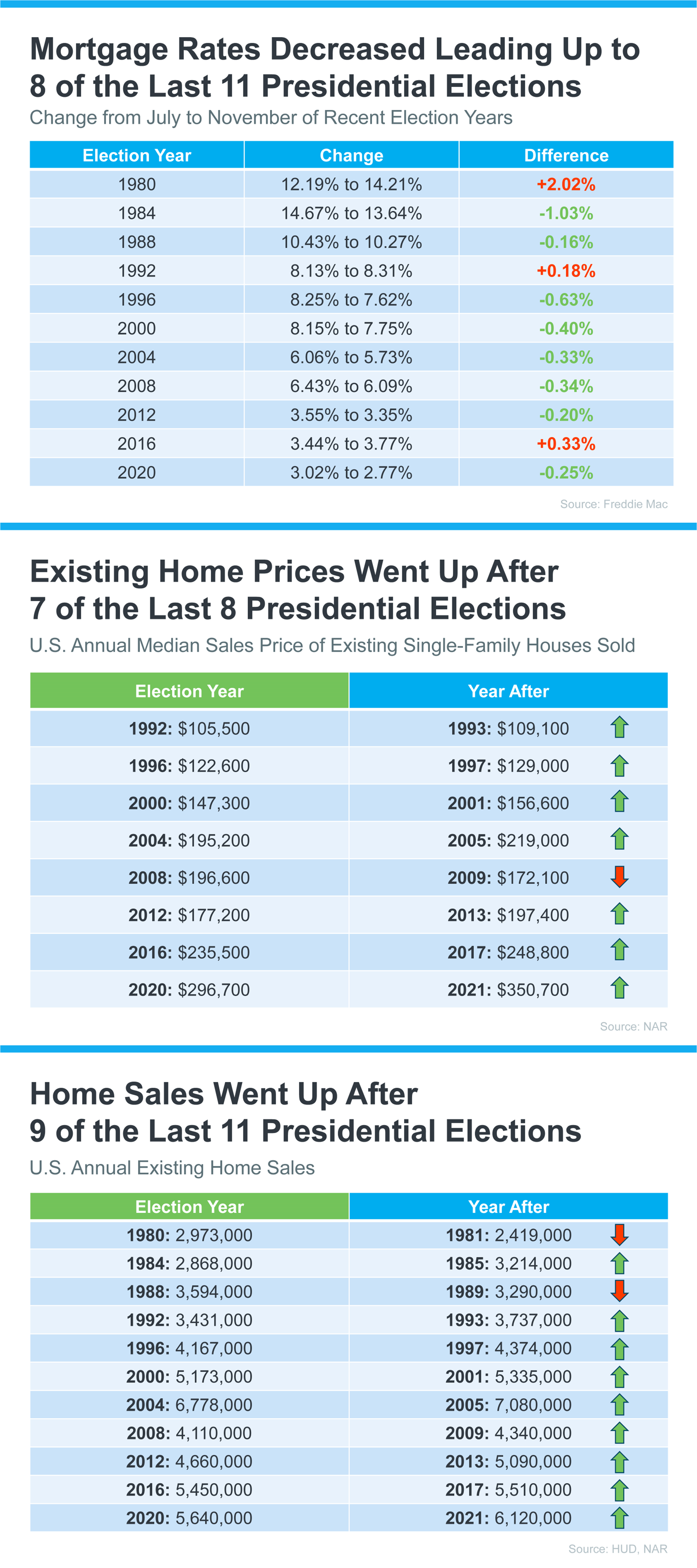

Another aspect to point out is the trends we typically see in post-election years. Historical data indicates increased closed sales, lower interest rates, and price growth. This data, coupled with pent-up seller demand and gradually decreasing interest rates, should drive sales to increase slightly and prices to appreciate and remain stable. Most homeowners are sitting on well-established equity, enabling them to make fluid moves.

If you or someone you know is considering buying, selling, or both, now is a great time to reach out. Executing a purchase and/or sale and a move takes strategic planning to achieve the best outcome. I love helping my clients identify their goals, curate a detailed list of items to create the ideal results, and help guide the process to a successful finish. A new year brings a fresh start, and why not start to verbalize, visualize, and start your planning now, whether your goals are immediate or in the distant future? Please use me as your real estate resource, as my goal is to be your trusted advisor rooted in data and market education.

As 2024 starts to come to a close, I want to spend some time talking about first-time homebuyers. Even if you already own a home, this is an important message to share; it can change someone’s life! In 2023, according to the National Association of Realtors (NAR) 2023 Profile of Home Buyers and Sellers, first-time home buyers represented 24% of the market share, which was down from 32% in 2022. First-time homebuyers are a critical part of the real estate market cycle, and we need to empower this group to invest in their future. They are also the audience that purchases inventory, enabling sellers to move on to their next home, which creates a domino effect as it travels up the market.

Often, first-time homebuyers purchase entry-level properties such as condos, townhomes, or smaller single-family residential homes based on affordability. It is also important to note that a buyer does not need a 20% down payment to purchase a home. In fact, according to NAR, the typical down payment for a first-time homebuyer in 2023 was 8%. There are loan programs that only require 3% down payments and even assistance programs requiring zero down. It is important to explore options so one knows their opportunity potential. For example, lenders will often advise borrowers to focus on saving vs. paying down debt in order to better qualify for a loan.

Sometimes, first-time homebuyers are able to skip that first level of home ownership and purchase a home that they plan to be in for many years, yet that is rare. I have found that it is critical that first-time homebuyers are focused on what monthly payment they feel comfortable taking on and commit to shopping at that price point. They then apply that price point to a combination of location, property type, and the condition/features they can afford.

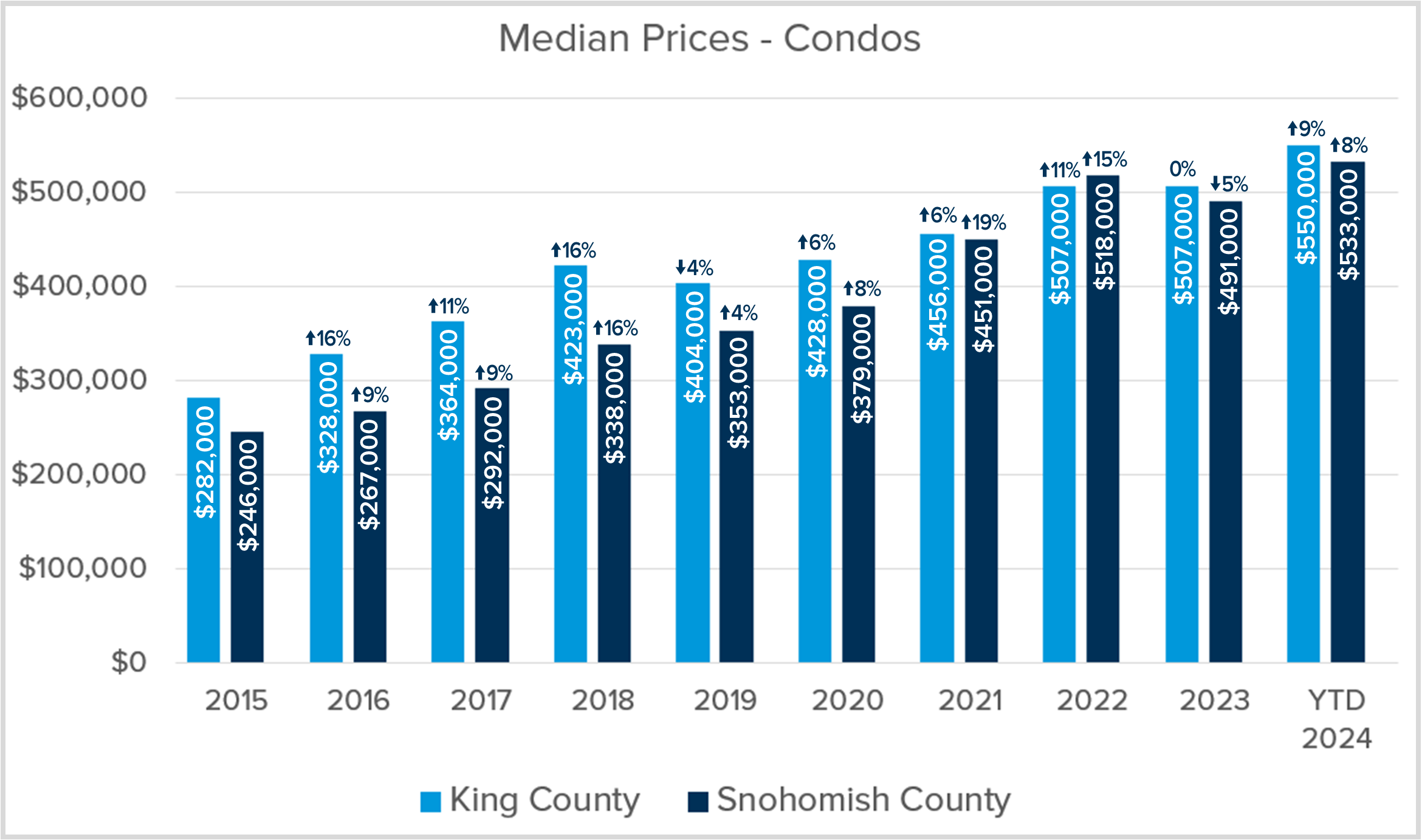

The primary benefit of ditching the rent payment and becoming a first-time homebuyer is getting on the trajectory of building household wealth. As you can see from the charts below, real estate has appreciated in both King and Snohomish counties over the last 10 years, whether it be a condo or a single-family residential property. This appreciation becomes a nest egg of savings for the homeowner over time.

For example, if you use the data from the Snohomish County Condo chart, a first-time homebuyer who bought a condo in 2020, the median price in the market was $379,000. That is now $533,000, which is a 41% gain. Granted, these are raw numbers and represent a 30,000-foot view of the market, which illustrates the trends. We can’t simply apply the percentage growth in the market overall; we would analyze comparable properties in the specific area of the subject property to find the accurate value. The appreciation trend, however, shows that the first-time homebuyer who bought in 2020 is now sitting on a healthy nest egg of savings to utilize to purchase their next home if they desire a different property based on life changes. Plus, there is no other investment vehicle that allows tax-free capital gains up to $500,000.

I point this out because I often encounter would-be first-time homebuyers who call off their search because they cannot afford the type of home or area they want, and continue to rent in the hopes of saving more to afford what they want later. While I would never want anyone to buy a home they don’t want, I do encourage my clients to consider what they can compromise on in order to start building wealth through homeownership sooner rather than later. Even if you apply the home appreciation for condos in Snohomish County prior to the pandemic, the median price in 2015 was $246,000, and four years later, it was $353,000, which is a 44% gain. Most people would not be able to save that much over that period of time, hence the advantage of building wealth via homeownership.

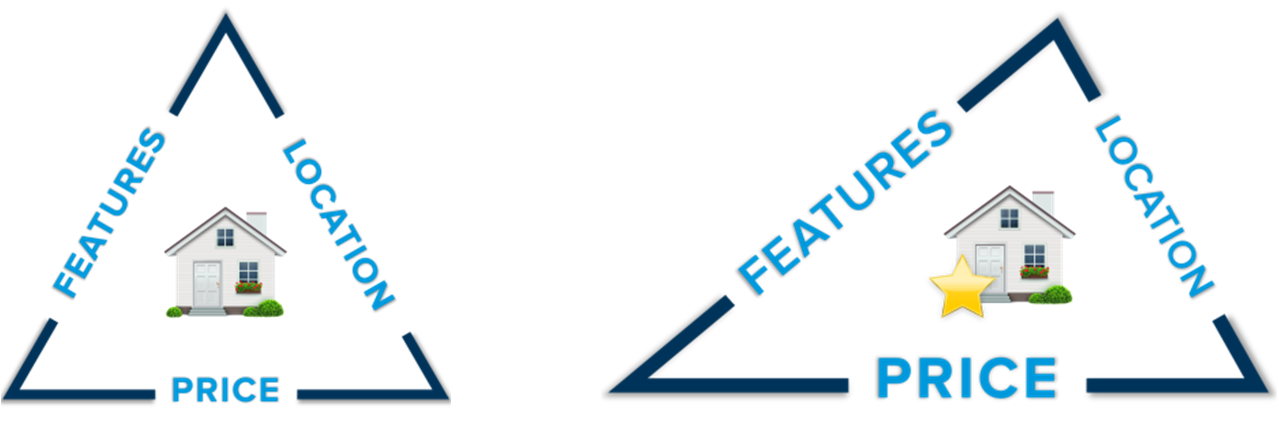

An exercise I often use with my buyer clients is applying the Triangle of Buyer Clarity to their budget and search. I am the first person to say that shopping for a home is exciting and even romantic, which results in starry eyes focused on dream homes and HGTV lore. I find that the quicker a buyer is able to put the dreaming part aside and get to the brass tacks of the market, the quicker they succeed in a purchase. Monthly payment is the single most important element to focus on to bring clarity to a buyer’s search. This figure should direct the price range for a buyer, which will determine which location, condition/features, and property type they can afford.

As you can see from the example of the Triangle of Buyer Clarity, buyers often have to adapt their search to meet their budget needs; it is rarely the perfect balance of an equilateral triangle. That could mean adapting by buying a townhome instead of a single-family home, going to a location that is a little further out, or being OK with a 90’s kitchen instead of a perfectly modern masterpiece. Getting into the market is more important than finding the perfect fit. The good news is that market trends show that townhomes, all locations throughout each county, and even 90’s kitchens appreciate! One could even tap into their equity down the road once it is built up and remodel that 90’s kitchen.

Homeownership provides many benefits. Wealth-building opportunities are huge because we all need a place to live, so why not pay your own mortgage and gain appreciation instead of building your landlord’s portfolio? There are tax benefits, too, as you can use the interest as a write-off. Plus, you get the freedom to make your house your own and build a community where you live. You can paint the walls and dig in the dirt, and you don’t have to answer to your landlord. Overall, homeownership provides stability, freedom, and community. Helping my clients gain tangible and intangible benefits is the primary goal I work towards.

This is why I couldn’t let 2024 end without giving a shout-out to the would-be first-time homebuyers out there. My best piece of advice if you are considering buying your first home is to come up with a plan. I offer all of my clients a buyer consultation meeting where we review the market trends, apply their goals and search criteria, get them connected with a reputable lender, and devise a custom plan for them. The plan could start right away or sometime in the future; what matters is working towards the goal.

My mission is to help people gain the benefits of homeownership when they are ready. When I hand off the keys to a first-time homebuyer, it is one of the most rewarding aspects of my job because I know we have changed their lives for the better. If you are a potential first-time buyer or know someone who is, please reach out, I’d be honored to help.

Your home is your shelter where you make memories, a large part of your financial nest egg, and a vehicle for creating wealth. Knowing what your home is worth is empowering and important. The reasons that may come up when you need to know your home’s value can have a direct impact on your financial health. Do you need to update your insurance, do some estate, tax, or financial planning, prepare for a re-finance, line of credit, or remodel, or are you considering a move? Relying on accurate home valuations for all of these endeavors will result in the best outcome.

To estimate your home’s value, you can easily jump on a public website that will spit out a value. This is called an AVM (Automated Valuation Model). There are a handful of free ones such as Zillow, Redfin, and RealEstimate. These sites are free for the consumer to visit and are based on a unique AI-generated algorithm that is typically a recipe of tax assessment data, CPI figures, market trend data, computer-picked comparable properties, and user-submitted data. They do not take into consideration important value points such as the condition of your home, improvements you’ve made, or nuances of the neighborhood; factors that only an actual person can evaluate.

It is important to note that on all three of these free sites, the algorithm and AVM tool are funded by the advertisers on the site, which are real estate brokers and lenders who want your business. The AVM is the carrot to get you in front of these high-paying advertisers who hope you click to connect so they can convert you into their real estate client. This is unlike the relationship-based business that I foster; this is more of a “sales-y,” transactional approach. Despite the sharks in the water, an AVM is a good starting point, like dipping your toe in the pool, but don’t get bit!

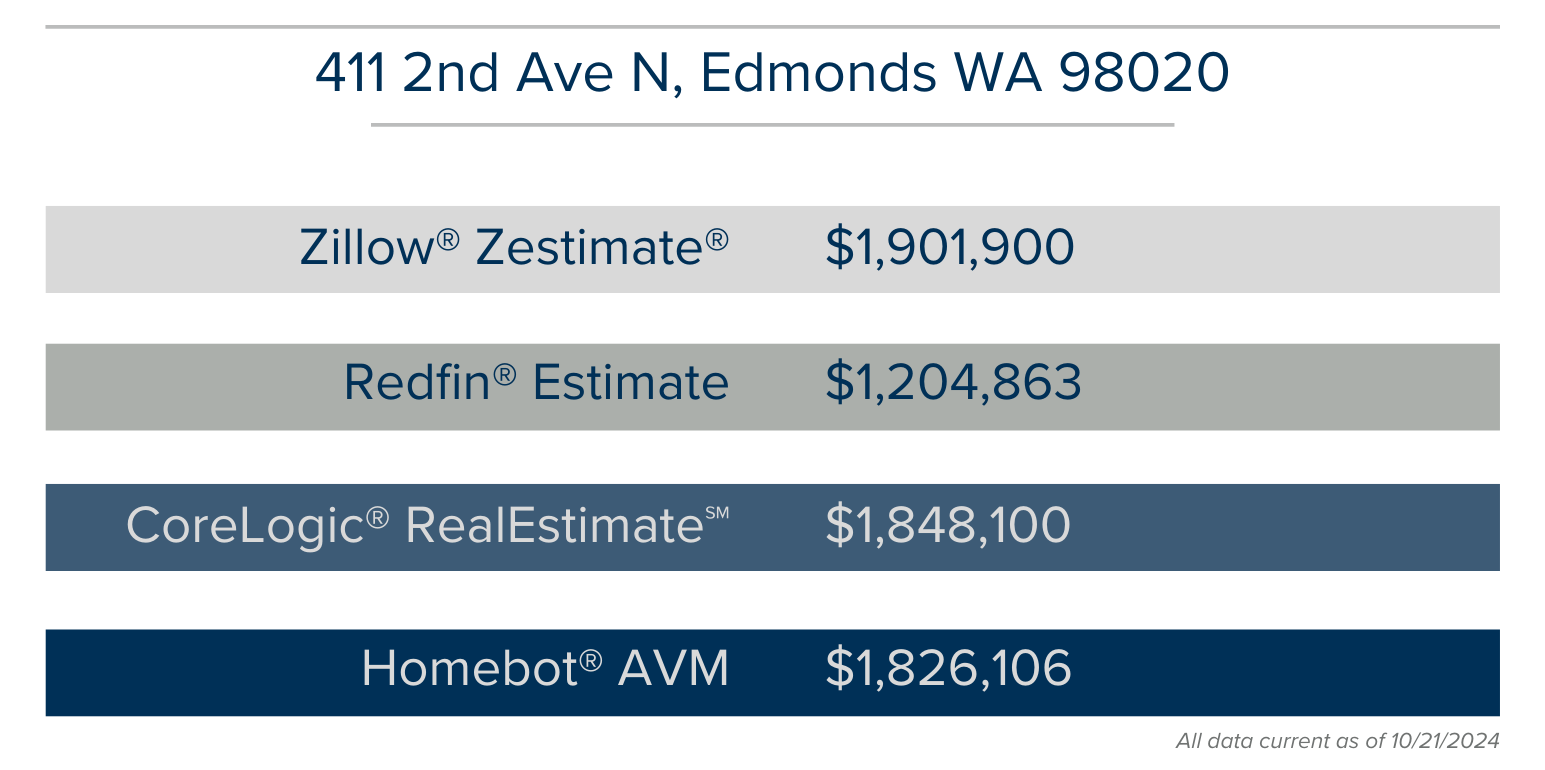

Here are the current AVM (Automated Valuation Model) values for a subject home from four sources (3 free and 1 fee-based). As you can see, the values vary. If you have a need to know the value of your home, don’t rely on an algorithm. According to Zillow, their accuracy varies by 7.49%; that is a huge variation! For example, that is $75,000, either high or low, for a $1M home. Depending on what you are planning for, that inaccuracy can severely cost you.

The AVMs above vary by 58%. If you apply the average Zillow accuracy percentage, the Zestimate® above could be off by $143,000 or more. It is important in this new world of AI that we do not underestimate the power of the human algorithm. Evaluating a home with all 5 senses, experience, and expertise is critical in establishing a home’s true value. Just like AVMs that vary, it matters who you align with, too. Hungry sharks who are paying to find clients, brokers who sell real estate as a hobby or side hustle, or brokers who are not engaged can all be detrimental. Seek out a professional who is committed to their craft, a student of the market, and up-to-date on market trends when you are assessing your largest asset.

If you want more precise information, consult a trusted advisor like me. By selecting accurate, comparable properties and analyzing today’s market trends, I will provide you with a much more comprehensive evaluation of your home’s value relative to its specific features, condition, and location. Please reach out if you are interested in having me tour your home and complete a Comparative Market Analysis (CMA) so you can plan for your future with confidence.

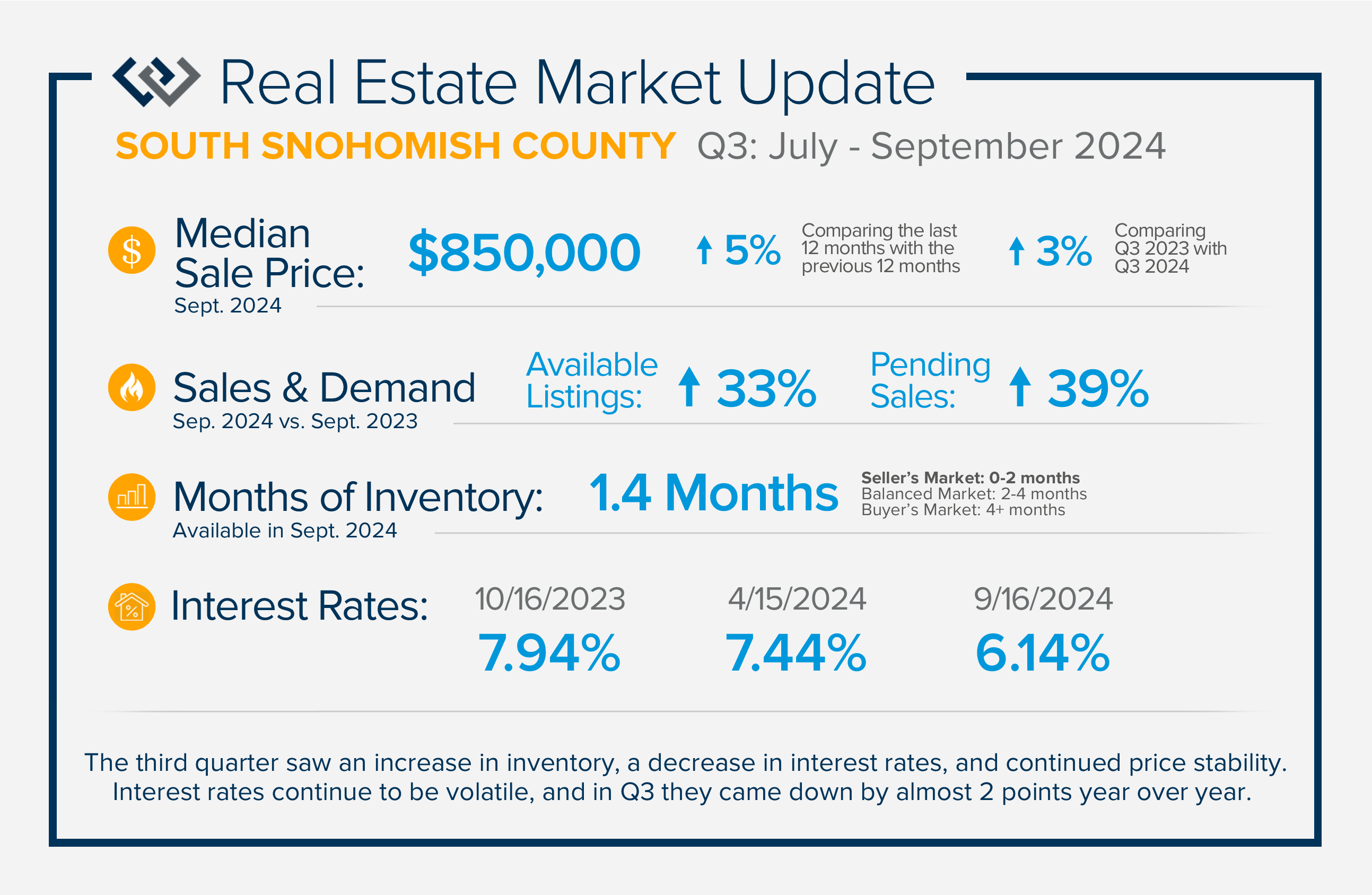

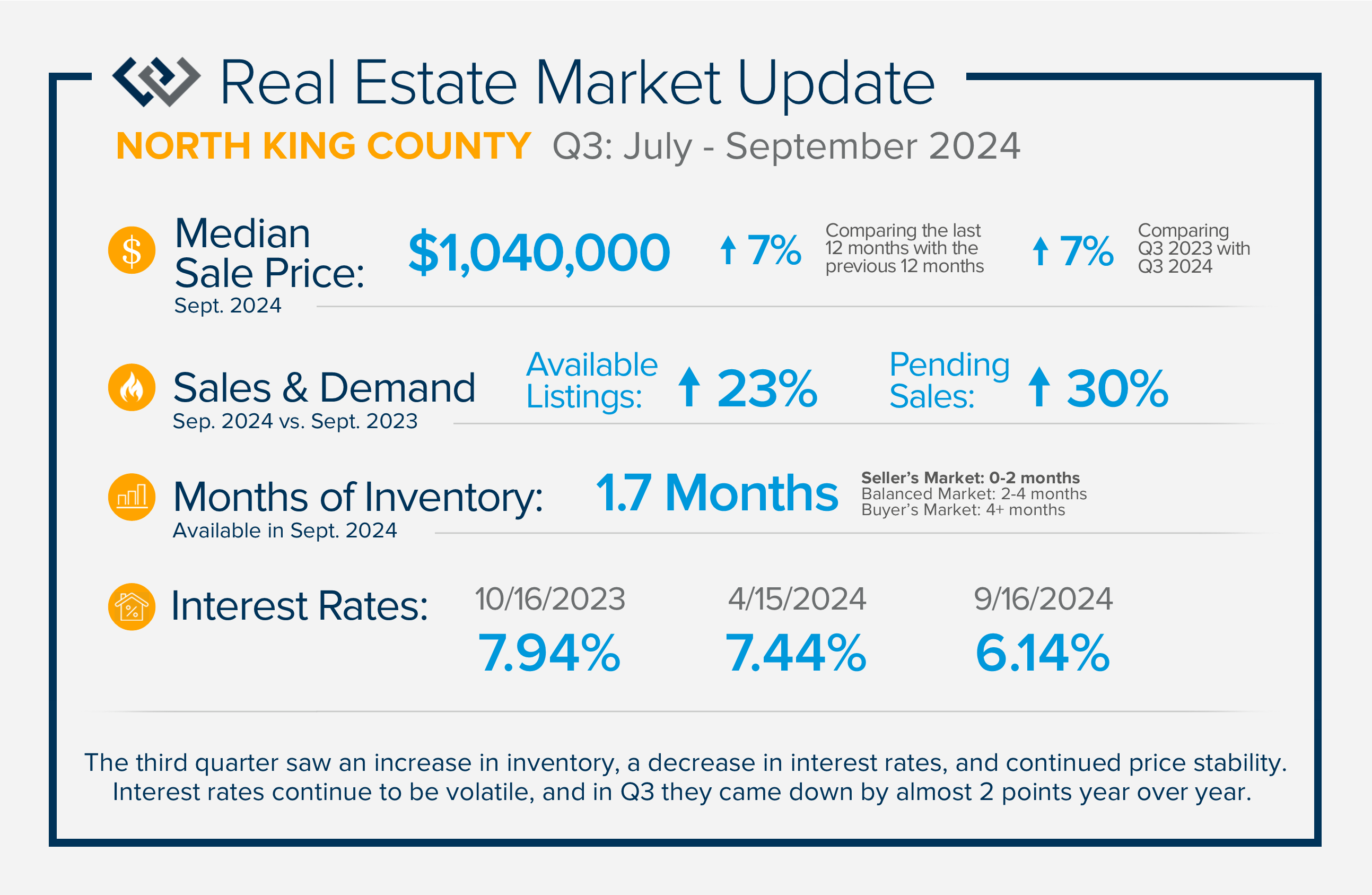

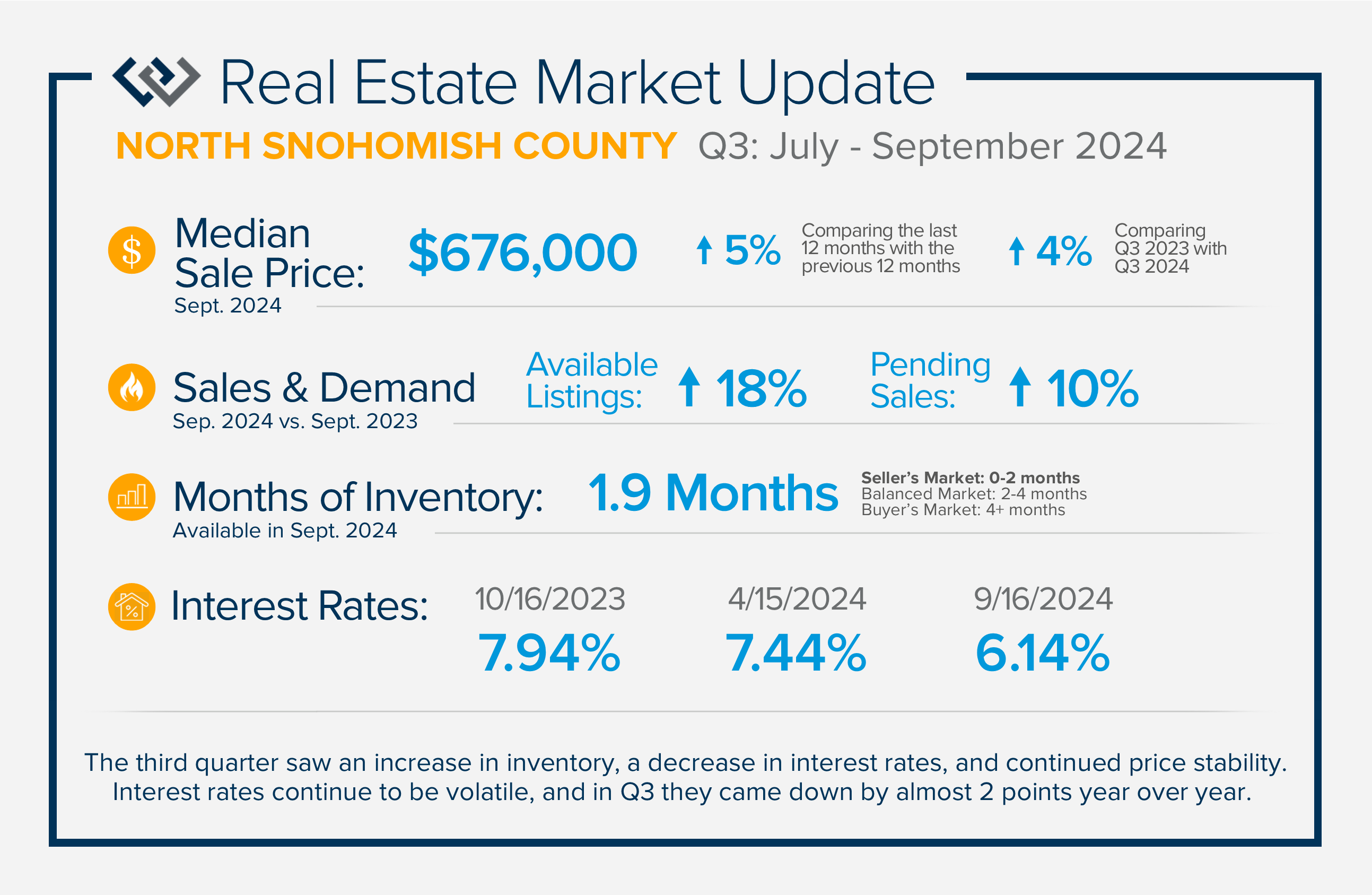

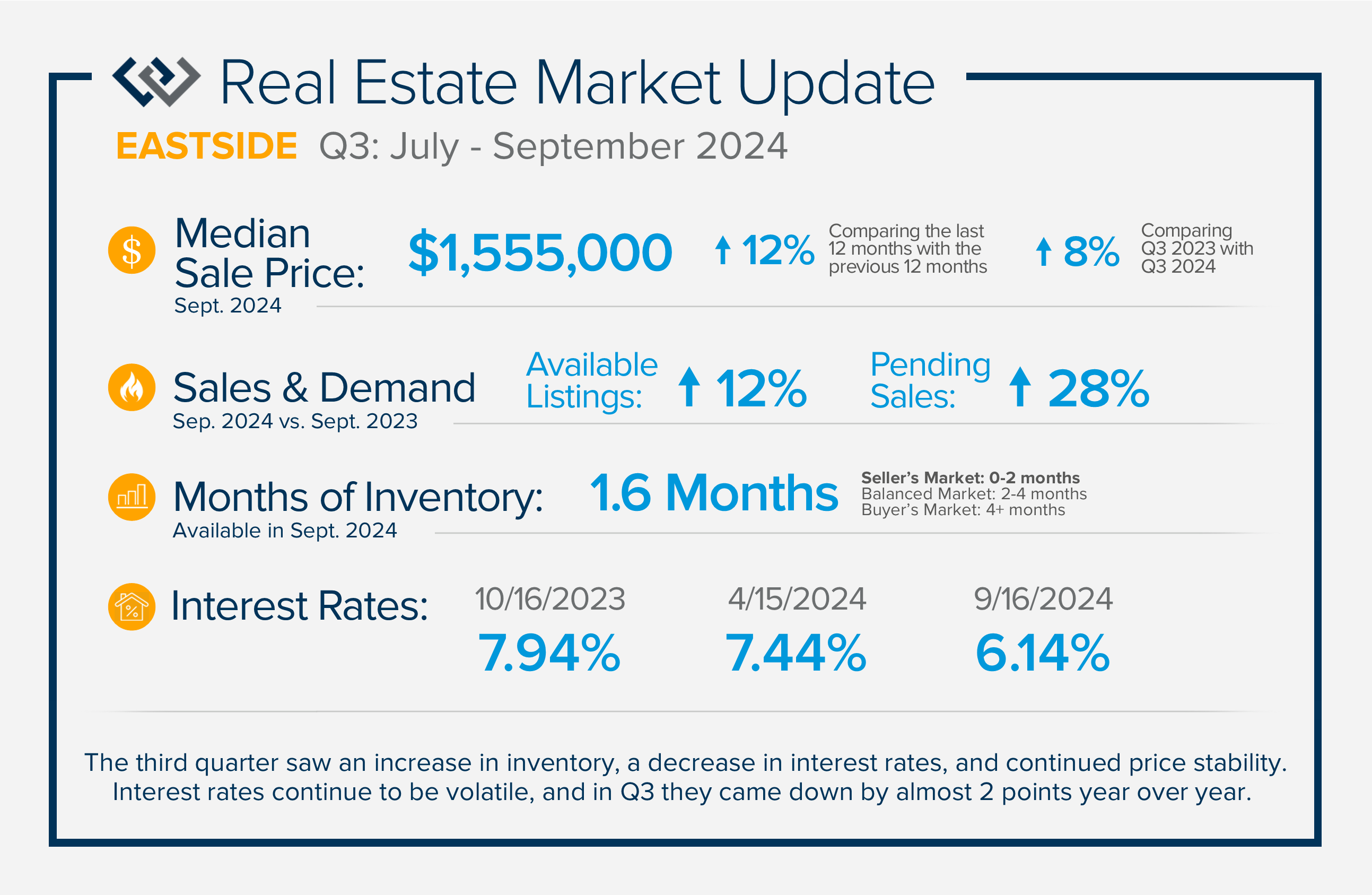

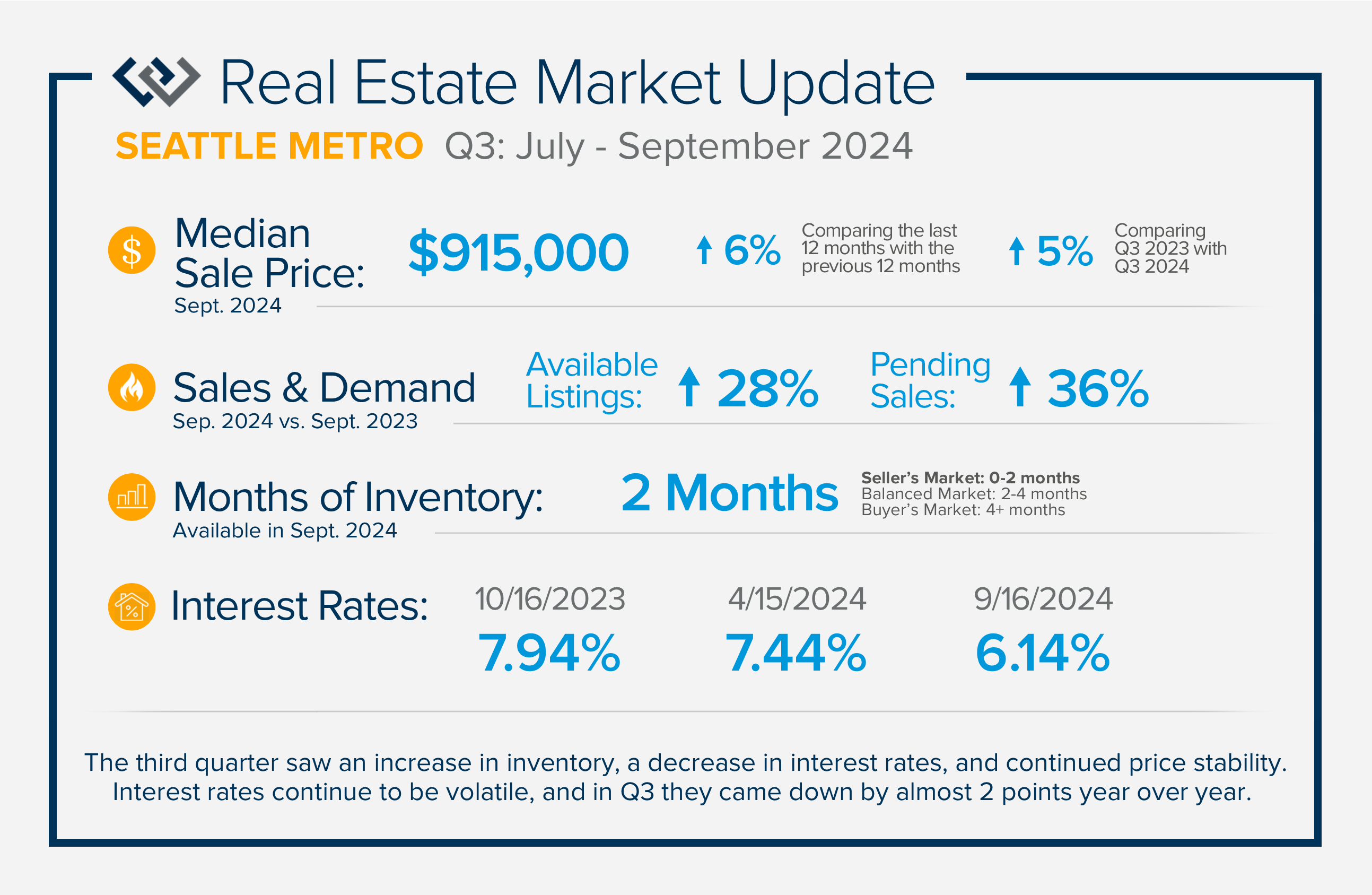

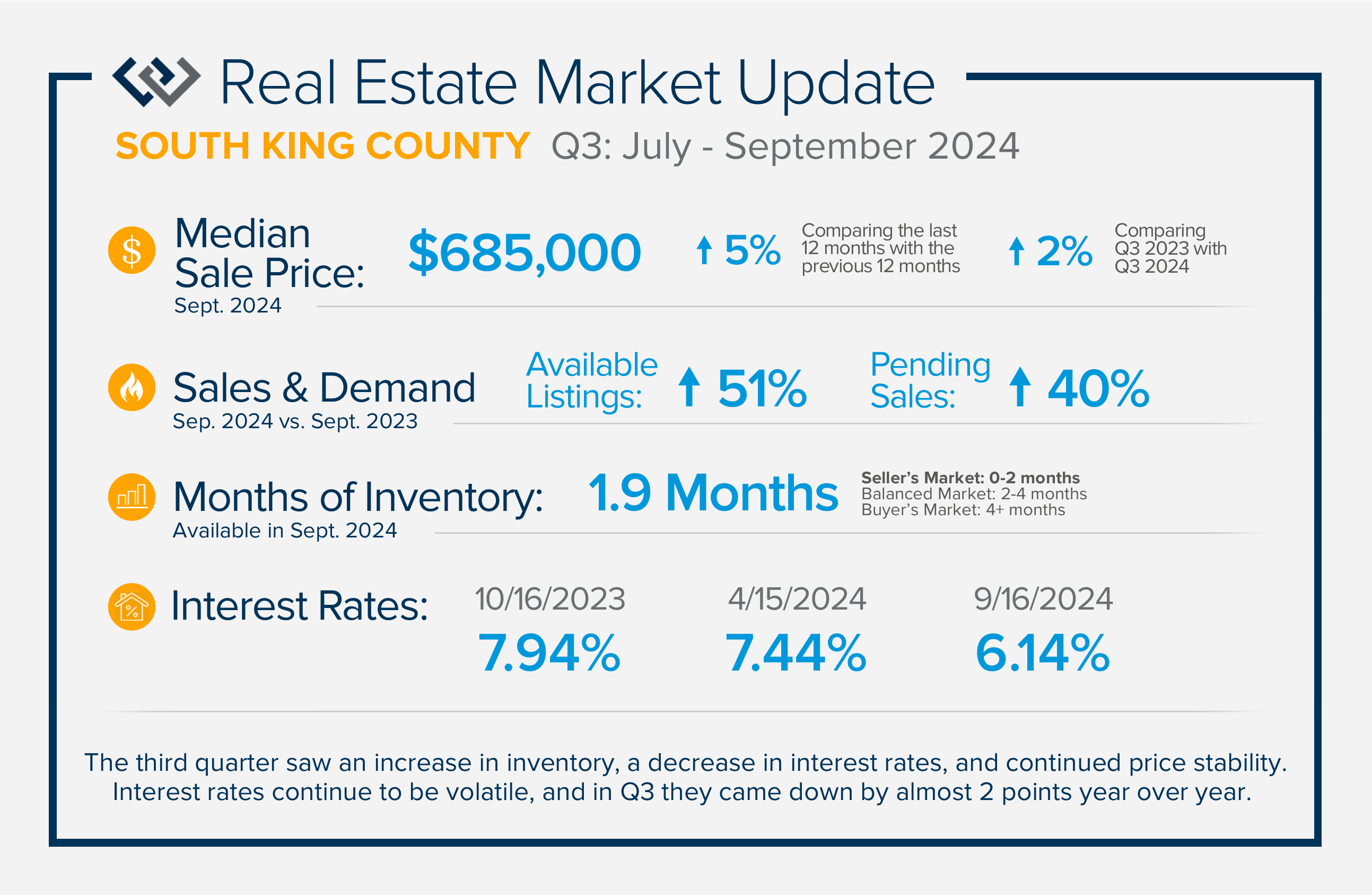

The third quarter saw an increase in inventory, a decrease in interest rates, and continued price stability. Interest rates continue to be volatile, and in Q3 they came down by almost 2 points year over year. This caused more buyers to enter the market and pending sales to rise. The number of available listings has improved after a very tight start to the year. Some sellers have been willing to forego their previous low rates for a new house, creating more movement in the market. The combination of lower rates and more selection should have buyers excited to make a move. Equity levels remain strong in our region as prices have remained steady and appreciated year over year.

If you are curious about how market conditions affect you, please reach out. I aim to educate my clients to empower strong decisions.

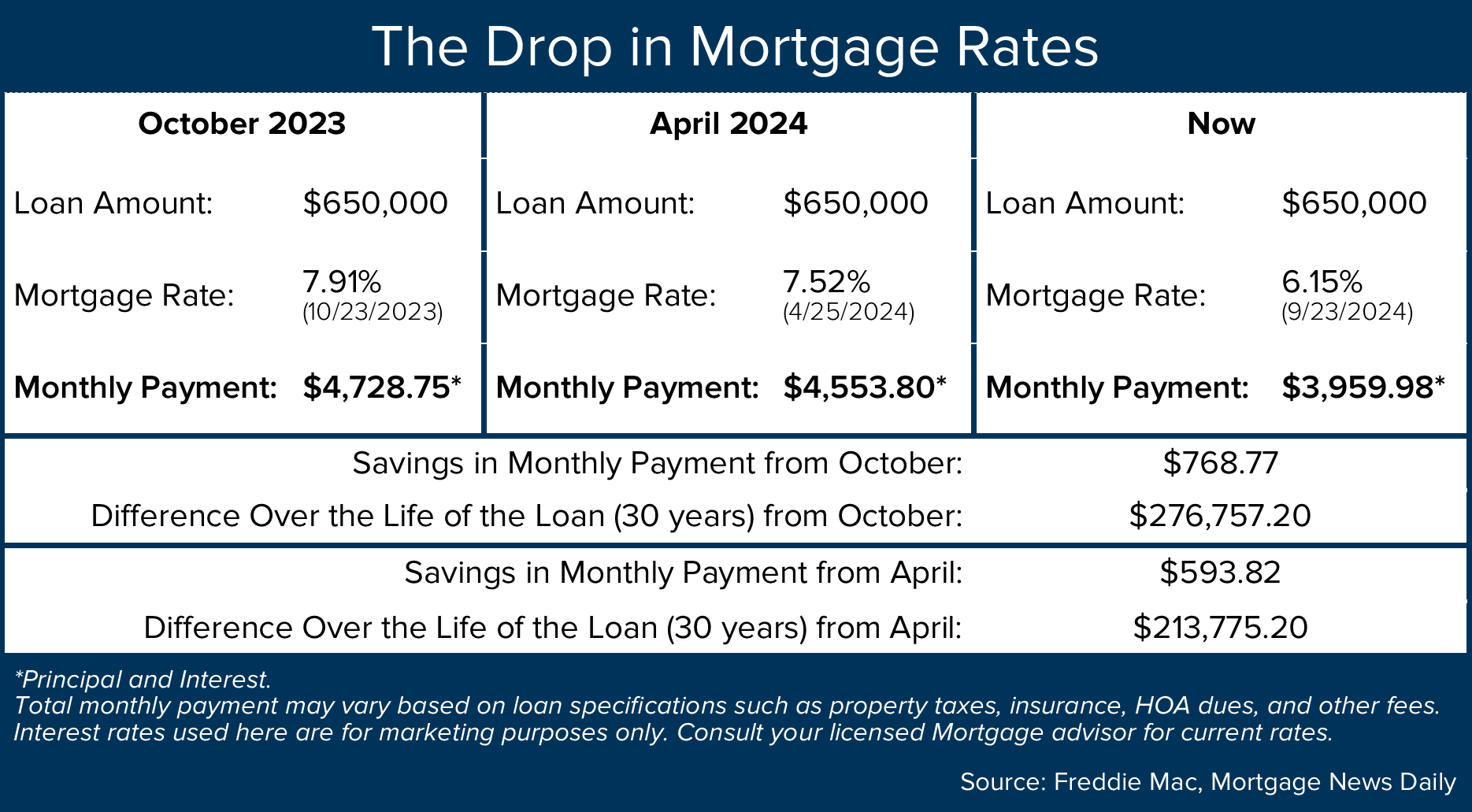

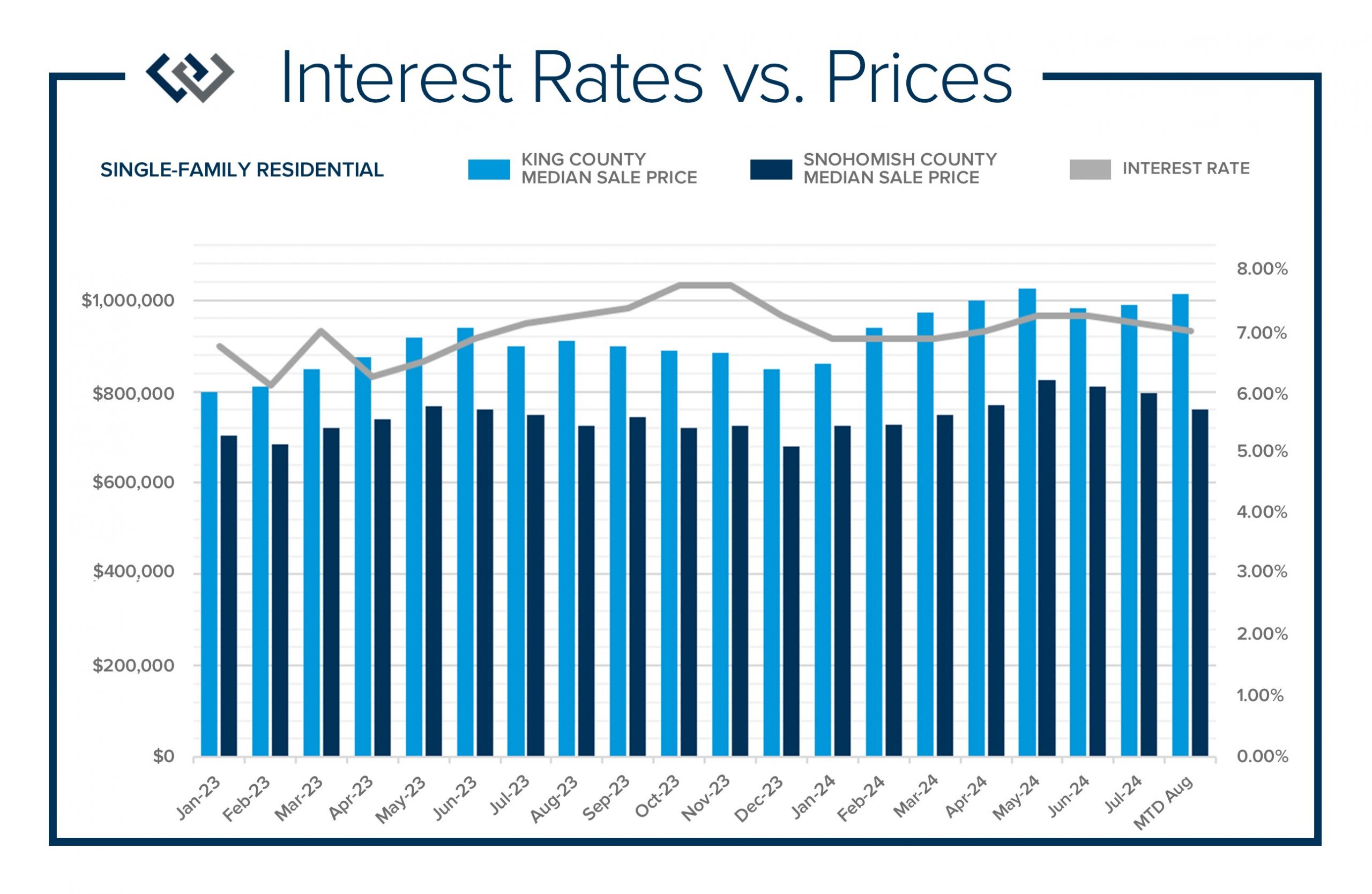

As we celebrate the start of autumn, the season of change, the leaves on the trees are not the only things that are falling. Interest rates have gradually fallen throughout the year. Just 11 months ago, rates were almost 2 points higher; in the frothy spring market, they were nearly 1.5 points higher. During this same time, the median price in King County and Snohomish County grew. In King County, the median price was recorded at $975,000 this August and at $775,000 in Snohomish County, which are both up 7% year-over-year from August 2023.

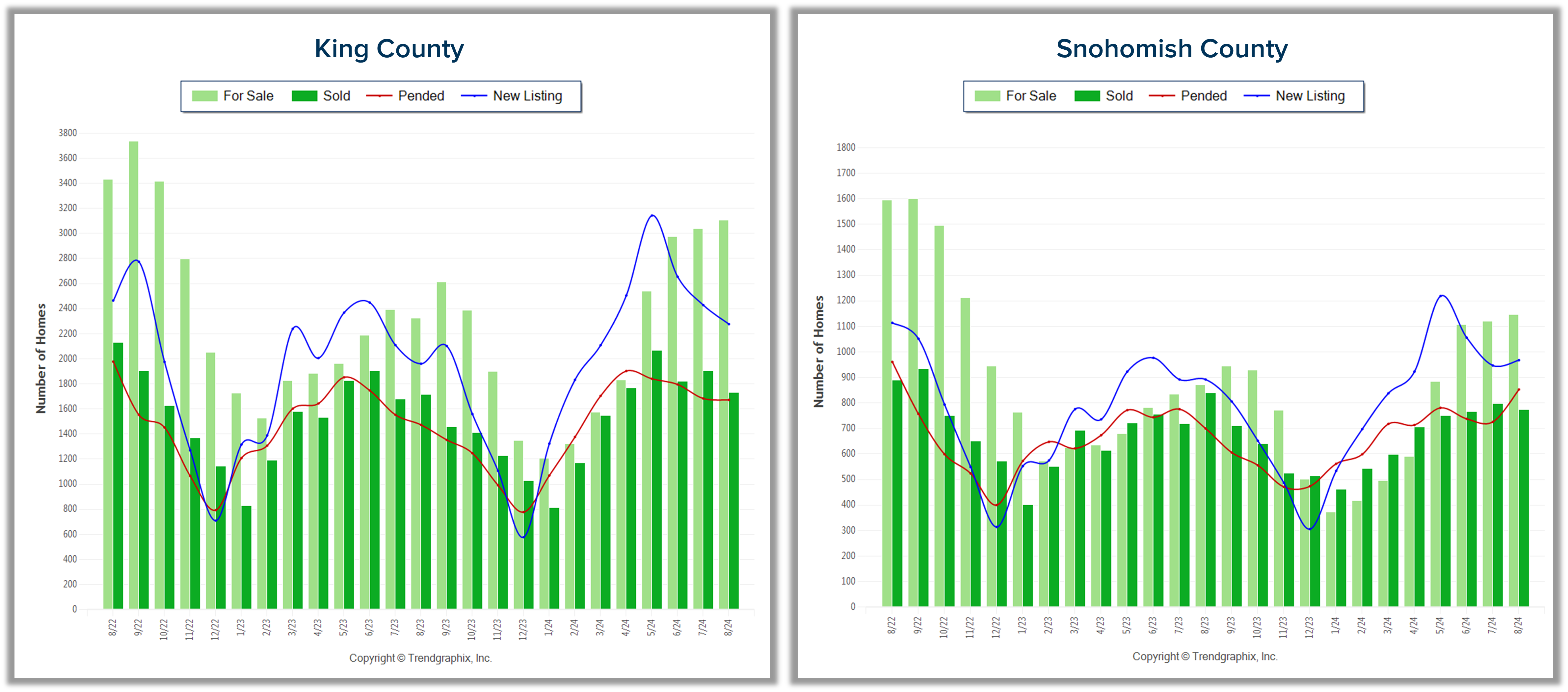

Another trend that we are witnessing is a rise in available inventory for sale. August recorded the highest level of available homes for sale since the fall of 2022, two years ago. There were 3,105 available homes for sale in King County in August 2024 compared to 1,207 in January 2024, and 1,147 in Snohomish County in August 2024 compared to 374 in January 2024.

The combination of lower borrowing costs and more selection should be a welcome change for buyers. When the inventory was much tighter in the first half of 2024 and interest rates were higher, prices were increasing at a rapid rate. We are starting to see new buyers enter the market and some who have sidelined themselves return. This indicates that prices will remain stable as we finish out 2024.

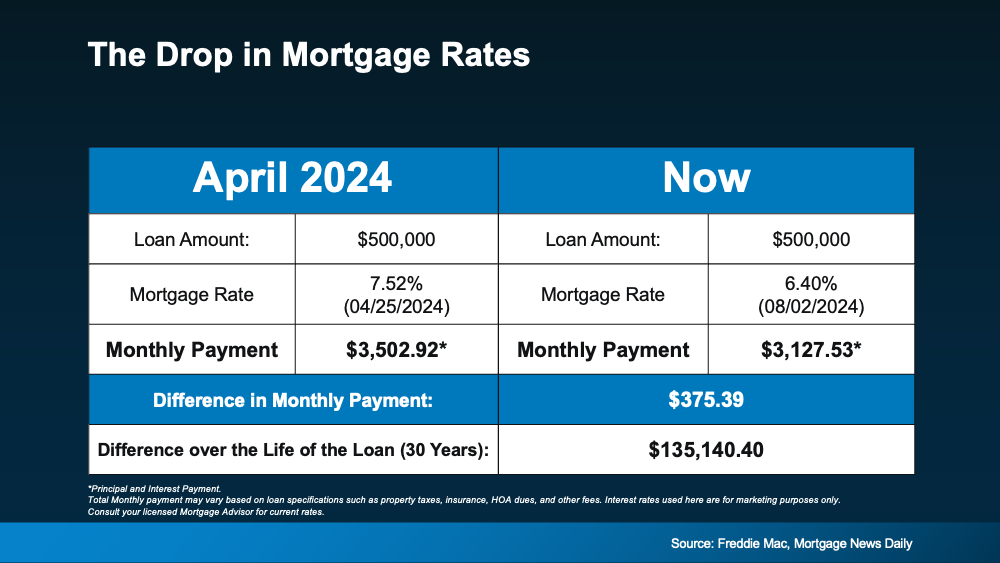

Currently, buyers have more selection and the opportunity to grab a lower monthly payment. As you can see from the chart below, buyers have a significant opportunity to afford a higher price point at a lower rate or stay at the same price point and have a lower monthly payment. The reduction in rate over the last year is reducing monthly payments and creating great long-term savings over the life of the loan. The rule of thumb for affordability is a 1-point shift in rate affects a buyer’s buying power by 10%. For example, a home priced at $800,000 with a 7% interest rate will have a similar monthly payment as a home at $880,000 with a 6% rate.

The hesitation I am seeing in the marketplace is a desire for rates to come down even further. The good news is that they are predicted to continue this gradual decline. Where I am concerned is a decrease in selection. If we look at seasonality, it is common for inventory to be low in the first half of the year, especially in Q1 (see the King & Snohomish graphs above). If rates continue their slide and fewer new listings come to market, buyers will find themselves duking it out in 2025. Right now, while there are multiple offers on some properties, there are more properties that are being negotiated into contracts with one buyer.

This has created a more nimble market, particularly for buyers who also have to sell their homes to reposition their equity into a downpayment. While tight inventory provides great leverage for a seller, many sellers are also buyers. Analyzing the market conditions to align the environmental influences to create the best possible outcome for your goals is paramount, and it will not be the same for everyone. Depending on my client’s goals, timing can vary.

Oh, and another sentiment I often hear is, “Will rates under 5% ever be back?” That is rather unlikely and will go down as a historic time in our economy. With that said, if you are in your “forever home” and you captured a historically low rate, kudos to you! Truly, so awesome! If you are not in the home that is right for you, now may be the time to curate a plan to get you into your next home. If homes were selling at a rapid rate and prices were appreciating this last spring with 10% less buyer power, I imagine next spring will be much of the same, if not more.

One final item to note is the election. History shows that post-election year markets are brisk with sales and experience price growth and rate decreases. I am paying attention to key indicators such as inflation figures, unemployment measurements, the gap between the 10-year treasury yield and mortgage rates, and our local market conditions in order to provide my clients with the most accurate and up-to-date information to empower strong decisions.

Are you curious how all of this affects you? Real estate is the number one tool for building wealth, and you also get to live there. I think that is pretty important, and I love nothing more than providing valuable insights, having strategic conversations, and helping people align their homes with their lives. Home is where the heart is and also where your nest egg has the most reliable long-term growth. Please reach out if you’d like to dig into the details and apply them to your housing and investment goals.

Summer 2024 welcomed an increase in available inventory, a drop in interest rates, and continued price stability, which has upheld strong home equity levels. After a double-digit ramp-up in price appreciation in the first half of 2024, prices have slightly come off the peak of May 2024 and found stability. This trend is historically consistent with seasonal patterns and nothing to be alarmed about.

Increased selection for buyers was a welcome relief as inventory was extremely tight in the spring. While there are still homes getting multiple offers and escalating, we have also seen some buyers make purchases contingent on the sale of their current home. The market has become a bit more nimble for buyer’s terms in some cases. It is important to understand the nuances of each location, product, and price point, as the environment can vary which would indicate whether a buyer would need to compete or be able to negotiate more.

These trends are coupled with rates dropping below 7% in June and they have recently sat in the mid-6%. Rates were a point and a half higher in October 2023; this is a great improvement! We anticipate rates slowly dropping further which will put upward pressure on prices. The Fed meets again this month and if rates come down even more, buyer activity will increase. Between the lower rates and higher inventory, buyers should be excited and ready to act!

As you can see from the chart below, this shift in rate directly relates to a buyer’s monthly payment. Homes are expensive, so the cost to carry a loan is critical. These recent drops are helping out and should be paid close attention to as buyers are payment-driven in most cases. The opportunity to secure a home now with today’s rate could mean a buyer could enjoy a stable price and choose to re-finance or adjust to a lower rate later keeping their same basis. Buyers should also understand that homeownership is a key component to building wealth.

I anticipate a healthy late summer and fall market. Over the Labor Day Weekend, buyer traffic was busy despite the holiday and activity is bubbling up. The lower rates are helping some folks jump off the fence. Even some sellers are getting ready to sell and relinquish their lower rate, so they can move to a home that better fits their needs. I’m excited about the real estate market for the remainder of 2024 and into 2025. If you are curious about how the trends relate to your goals, please reach out. I am committed to staying connected and up-to-date on the latest trends so my clients make well-informed decisions.

Higher-density housing is happening in our state and quite possibly right in your own backyard. This is called middle housing. Middle housing is a term for buildings that are compatible in scale, form, and character with detached single-family houses. In 2023, House Bill 1110 was passed in a bipartisan 35-14 vote in the Senate and 79-18 vote in the House, and is likely to affect most homeowners and purchasers by the summer of 2025 when state law requires local municipalities to enact changes to their local codes.The state’s intention behind HB 1110 is to help provide more affordable housing options in the wake of the Washington State housing affordability crisis, which in turn, creates more density. It has been over a year since this was enacted and municipalities are starting to process and absorb these changes, and middle housing is coming to life.

Some items to consider are listed below:

Cities with more than 75k people must allow 4 units per lot; they must allow 6 units if within a quarter mile of a (major) transit stop, among other rules.

Cities between 25k-75k must allow 2 units per lot, among other rules.

Cities with fewer than 25k have to allow 2 units per lot.

Cities may not enact standards for middle housing that are more restrictive than for single-family housing.

Cities may not require off-street parking as a condition of permitting.

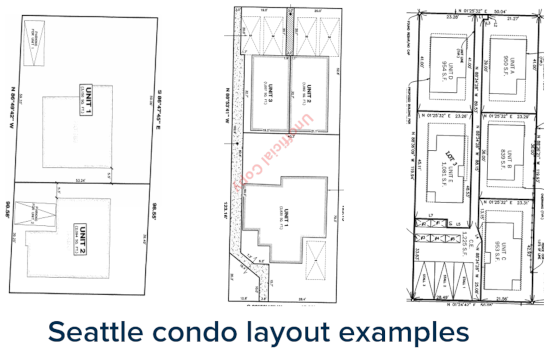

Putting political opinions aside, I want to help bring understanding to this option for homeowners and potential homebuyers. The call for higher density has allowed for some properties to be condominium-ized (creating units) vs. subdivided lots in order to add Accessory Dwelling Units (ADU). This is a much simpler process that can be done on smaller-sized properties vs. the larger lot requirements of subdivision. These ADUs can either be attached (AADU) or detached (DADU) and it depends on the size of the property and the location. Here is an example of what one could look like in the City of Seattle.

The City of Seattle has building guidelines that align with creating this density more easily via smaller building setbacks and tax requirements. Other cities have more restrictive requirements, it is location-dependent on how this will play out. Additionally, if a neighborhood has Covenants, Conditions, and Restrictions (CC&Rs) that were recorded before HB 1110 went into effect that prohibit ADUs, then this development will not be allowed despite the legislative change. Assessing this development potential starts with researching CC&Rs (if applicable) and inquiring with the city and/or county planning department where the property is located.

If a property is eligible for this type of growth, getting the condominium approved is a rather quick task. The condo map and declaration need to be drafted and recorded to be official and can take anywhere from 6-10 weeks depending on the responsiveness and availability of a qualified surveyor. The map will address the number of units, where they are located, Common Elements, and Limited Common Elements. The total cost for creating and recording these documents hovers around $10,000 and requires the services of a surveyor and experienced attorney.

If a homeowner is not ready to execute these plans right away, that is OK. They can stop at the recording step and would be grandfathered in to execute these plans in the future even if the municipality changes its building requirements down the road. Of course, many more details are involved, and hiring experts to help navigate the creation of these documents and development is key. Some homeowners are taking the step to create a condominium on their property to expand profitability when they go to sell, and some want to create multi-generational housing options for their families.

The point of this information is to elevate the awareness around these housing options and for homeowners to understand how to maximize the potential of their asset. It should also provide hope for some home buyers who think they are priced out of the market knowing that more of these housing opportunities are coming. If you are curious or have specific questions related to middle housing, please reach out. I have access to experts in the field who I can connect you with, so you can obtain accurate information. As always, it is my goal to help keep my clients well-informed and empower strong decisions.

Home values had positive growth in the second quarter of 2024, and inched close to the peak levels we saw in Q2 2022 before the post-pandemic housing correction. Despite inflation and interest rates remaining stubborn, demand has continued to be strong, resulting in a seller’s market.

A bright light for buyers is the recent uptick in new listings, which has opened up more opportunities after starting the year with minimal selection. Additional inventory will cause home prices to stabilize after rapid growth over the last six months. The average homeowner has close to 60% in home equity resulting in great returns when making a sale.

If you are curious about how today’s market relates to your real estate goals, please reach out. It is my goal to educate, inform, and empower strong decisions.

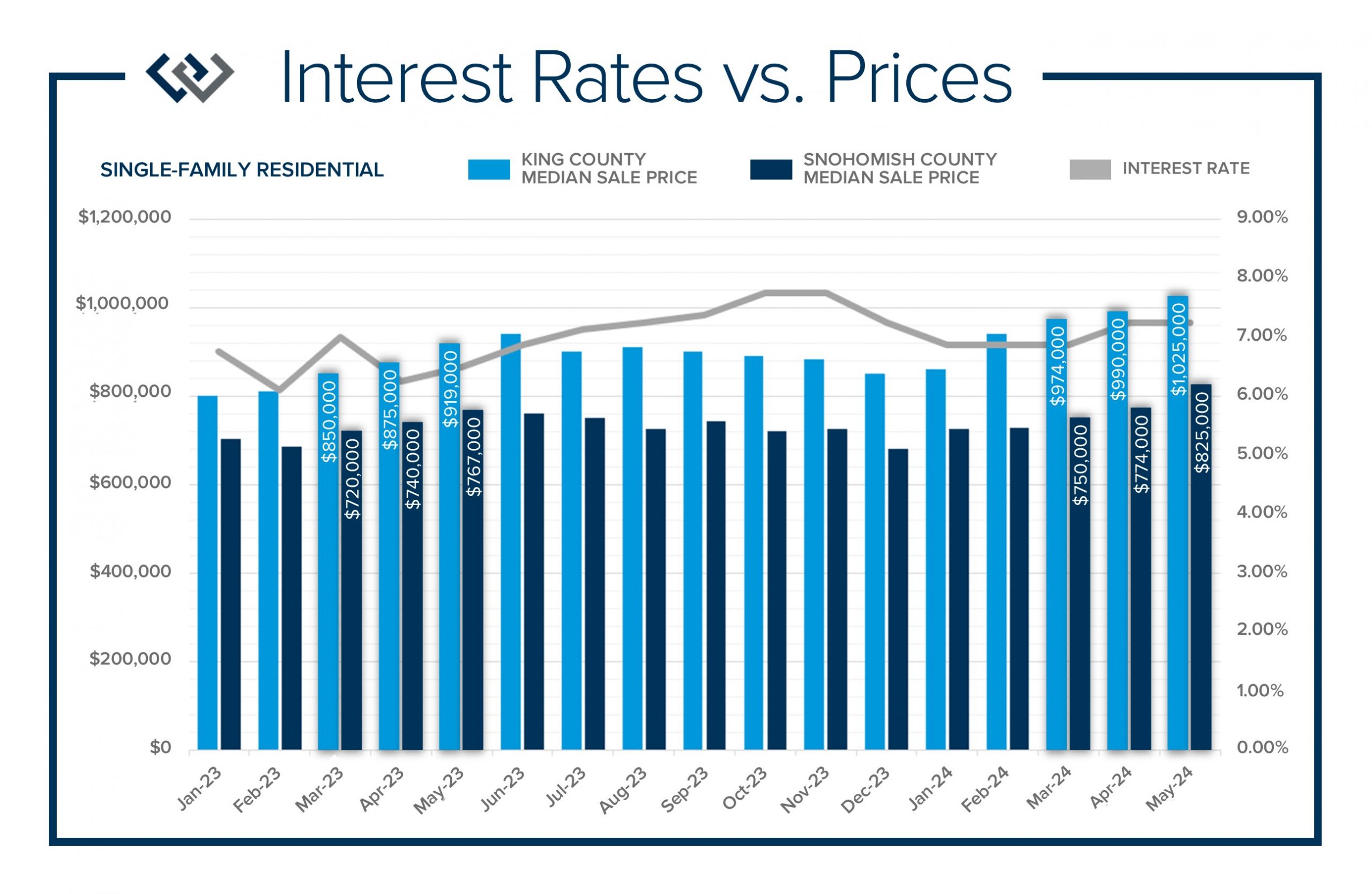

As we approach the mid-point of the year, I want to take a moment to explain all that has happened in the 2024 real estate market and where we might be headed. We have had strong price growth since December 2023, and in May 2024 prices matched the peak we saw in spring 2022. The interest rate increase and inflation-induced correction that took place in the spring of 2022 has shown very strong signs of recovery and stabilization. The chart below shows the last 17 months of median prices in both King and Snohomish Counties and also tracks the ebb and flow of interest rates.

Despite interest rates fluctuating between 6.75-7.5% from January through May 2024, price growth has been on an upward trajectory. Most recently, rates have hovered close to 7%. Inventory started the year very low! In King County, there were only 1,324 new listings in January and 534 in Snohomish County. This trend continued throughout Q1 2024 and has started to increase in Q2. In May 2024 there were 3,245 new listings in King County and 1,272 in Snohomish County. That was a 145% increase in King County from January to May and 138% in Snohomish County. Markedly, there was a 27% jump in new listings from April 2024 to May 2024 in King County and 34% in Snohomish County.

Adequate selection for buyers was limited, which drove prices up over the past five months. Buyers are starting to see some relief! There is healthy net in-migration into the Greater Seattle area, a stable job market, and the Millennial generation is out in force making their first purchases and some even moving up from their first homes. Since December 2023, the median price in King and Snohomish Counties has increased by 21%. One must take seasonality into account which elevates that growth, but there has certainly been a recovery in home values in the correction. Sellers are sitting on tons of equity as it was measured in November 2023 that homeowners in King County had at least 60% home equity and 57.5% in Snohomish County. This figure does not take into account the price growth we have seen in 2024 thus far.

So, what does all of this mean going forward? We typically will reach our seasonal peak in prices in May or June. This phenomenon is a result of price growth decelerating due to inventory growth over the second half of the year. The rate of price growth will slow as more homes come to market; this is not price depreciation, but deceleration. Homeowners are standing on the shoulders of immense growth over the last 5 months and need to keep that and the long-term growth in perspective. If the rapid rate of price growth continued, it would not be sustainable and would create market volatility. Moderation and price stability benefit the overall health of the real estate market and economy over prolonged extreme price increases.

As we head into the summer months, I anticipate more selection for buyers which will temper price growth. Sellers will enjoy the gains that have been made over the last 2 years and so far in 2024, not to mention the last 10 years. The recent increase in inventory has given buyers more opportunities to make a move. The constriction we started the year off with was restrictive for some buyers to enter the market and we see that changing. Buyers who were discouraged earlier this year may consider re-engaging so they can benefit from the increase in selection.

As far as interest rates, experts predict they will slowly recede and be dependent on inflation calming which has been stubborn. Affordability has been a dance of balancing home prices, rates, and monthly payments. Some buyers have been creative with rate buy-downs to manage the monthly expense, and some are purchasing based on today’s rates with the hope of re-financing in the future. A sound piece of advice for buyers is to buy based on payment, not on the peak of what you can qualify for. Your monthly output needs to be sustainable and somewhat comfortable to make sense.

Real estate is an investment and a key component to building wealth. While it might seem scary or risky to make a purchase, the long-term gains are favorable in comparison to other investment vehicles. Plus, you get to live in your home, love your home, and make memories in your home while it creates a nest egg. Life changes create reasons to move. Assessing where you want to be and how it matches your lifestyle is where the decision-making starts. If you have experienced some life changes and are curious about how the market relates to your housing goals, please reach out. It is my goal to help keep my clients informed and empower strong decisions.

Facebook

Facebook

X

X

Pinterest

Pinterest

Copy Link

Copy Link